BLOG

Data Now, Fewer Losses Later:

Optimize Your BNPL Data Strategy

Buy Now, Pay Later (BNPL) products have exploded across the globe, offering a new spin to point-of-sale (POS) financing for both consumers and businesses. From 2019 to 2021, BNPL loan originations increased by 970% from the top five lenders alone, and the industry continues to expand to include new verticals such as auto repair, grocery purchases, airline ticketing, and more. Consumers are beginning to rely on BNPL for everyday costs in order to help manage their cash flow. But none of this would be possible without data – more specifically, a strong data supply chain.

If you’re a BNPL provider, the data supply chain is the powerhouse for your solution. When you have the right data, you can better determine risk, protecting your business against fraud and loan default.

BNPL data strategies look beyond traditional data like credit scores and use alternative data to make credit more accessible and faster to approve without increasing your risk. While this allows you to expand your customer base in a secure way it also adds complexity to your data needs. So, how do you build a BNPL data supply chain strategy that gets the right data to the right place exactly when you need it?

Building Your BNPL Data Supply Chain

We know every potential BNPL customer must go through a process, but what does that process look like? Each step is built with different data checks that tell your decisioning engine whether to move that customer forward. An optimized data supply chain pulls only the necessary data needed for a customer at each checkpoint – data that comes from your data integrations and data partners.

An optimized data supply chain has these hallmarks:

- Multiple steps with distinct requirements

- Multiple checkpoints at which consumers either pass or get denied

- Steps that increase in complexity and cost of data

- No unnecessary data is exposed and paid for before you need it

Launching with an MVP:

Are you a startup launching your first BNPL solution? A finserv expanding your product line? Maybe you’re an online shop looking to reach more customers. Whatever the case, when building a new data supply chain for your BNPL offering or optimizing an existing one, you should begin with your minimum viable product (MVP) – the basics you know you need to launch your product.

An MVP has the least amount of checks in the process, pulling in the least amount of data. You might want to begin with an MVP if you want to:

- Go to market quickly

- Minimize the cost of development

- Analyze basic performance to optimize more complex iterations in the future

To launch with an MVP approach you’re going to need data to support three key areas:

- Regulatory compliance checks like KYC/AML

- Identity verification

- Credit risk

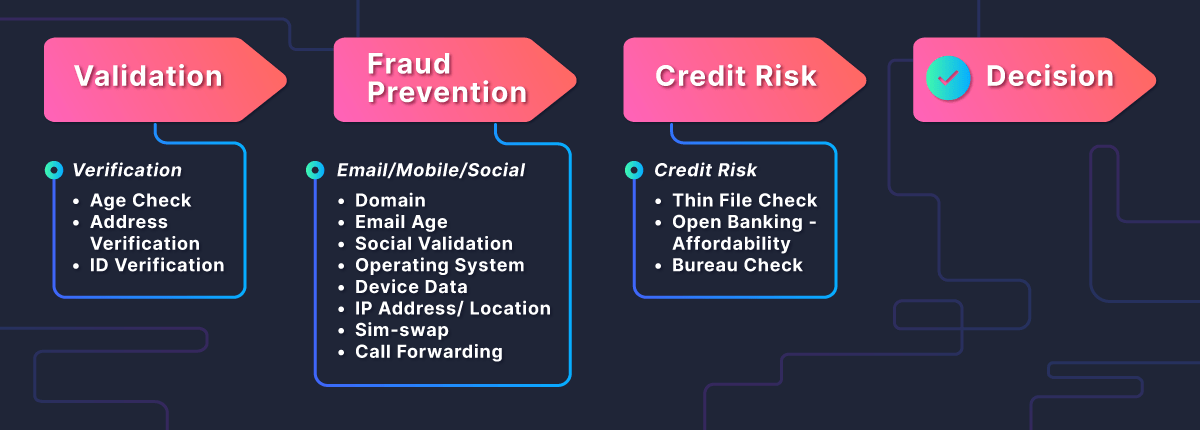

An MVP for consumer lending could look like this:

Step 1: KYC

The first step of the process is validating the most basic data to confirm the customer’s age, address, and identification. If you can’t verify a person’s ID, you certainly can’t lend to them.

Step 2: Fraud Prevention

The second step digs deeper into a person’s identity to ensure they are who they say they are and help prevent fraud. There is a wide variety of data you can pull for a fraud check, including email address verification, if a SIM card has been swapped, and other behavioral and alternative data. If not all of this information matches, it could be a sign of attempted fraud, and the person would be rejected.

Step 3: Credit Risk

The final step is to check creditworthiness. A bureau check is done through a soft credit check that grants you access to a consumer’s credit score without impacting it. With an MVP, BNPL providers would likely reject anyone with a score below a certain threshold or someone without enough credit history to have a score at all. If a person has made it through the process, the data is assessed holistically by a decisioning engine to determine whether and at what terms to grant the loan.

Beyond the MVP: Optimizing Your Data Strategy

Beyond the foundation needed for an MVP launch, you can optimize your supply chain based on your company’s risk appetite and goals. Before updating your data supply chain it will help to:

- Analyze success against your goals

- Identify weak points in your data strategy

While you may want to initially launch your BNPL solution using an MVP, as you grow and want to add complexity, you can incorporate new data points and data partners. Think about the kind of customer you want to capture, as well as business goals and preventative measures you may want to take, and ask yourself:

What percentage of fraudulent applications is our current process letting through? Is this in line with our business goals? If not, look to:

- Add additional fraud checks on existing steps

- Add standalone fraud prevention steps to the process

- Amend data sources to optimize as you go

Are we offering the most competitive terms to our customers? How can we improve conversions? For competitive edge and increased personalization, use data such as:

- Behavioral trends

- Geolocation

- Activity and usage

How effectively are we reducing defaults? Are we filtering out non-viable customers at the right point in the process? Make sure your flow features:

- Prescreening

- Scoring

- Additional data checkpoints on existing steps

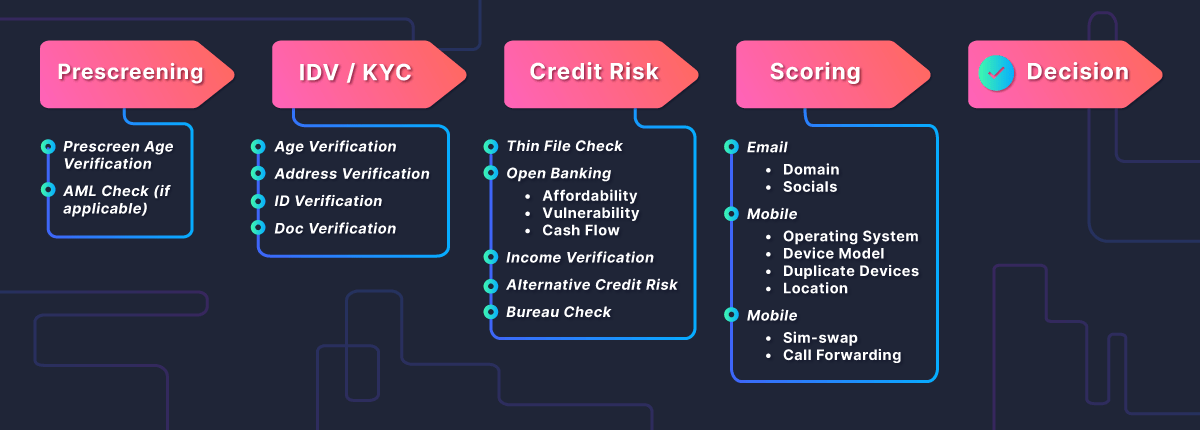

For BNPL providers that want robust data supply chains across credit, identity, and fraud while maximizing efficiency, an optimized flow could look like this:

Prescreening

Prescreening breaks down the identification verification steps even further, making sure the minimum requirements are met. It’s a faster, more efficient way to filter out unqualified applicants without using unnecessary time and resources.

What does prescreening look like in an optimized supply chain? Say you have a person under 18 – they’re not legally allowed to take out a loan, so their application would be rejected. In an MVP, someone that can’t even use the product would still have their identity verified, but it’s a waste to run those checks, since they’re not a viable customer. Optimization ensures you expose only the data you need at each step.

Scoring

Scoring pulls supplementary data that helps paint a clearer picture of a consumer’s risk. This includes mobile device data, additional fraud checks, or any other kind of alternative data you want to feed into your decisioning tech.

Why include scoring in your process? Again, it comes down to building your process for optimal efficiency and minimal cost. At this point, you would know if the customer was viable, who they are, and what their financials look like – this is all straightforward data to pull. Scoring adds behavioral information that is more time-consuming and costly to analyze and should be incorporated only when everything else checks out.

Ultimately, the more relevant data you have, the more accurate your decisions will be, the better you can predict future defaults, the easier it will be to identify upsell and cross-sell opportunities – whatever your business goals, the right data can help you get there. Optimizing your consumer BNPL supply data chain is dependent on finding the ideal number of checks and steps to accurately determine creditworthiness and risk, while keeping the process fast and efficient.

Ready to launch and expand your BNPL products? Look out for these data supply chain challenges

As BNPL products continue to grow around the world, new markets have emerged, and with them new challenges. To build a global supply chain, you have to know regional regulations, vendors, tech requirements, and more. Some of the challenges that can slow down deployment of your data strategy include:

- Identifying relevant local data sources

- Negotiating multiple contracts

- Complying with varying regulations

- Ensuring data privacy for different regional requirements

- Normalizing data formats

- Building and maintaining integrations

- Supporting global strategies

BNPL is a fast-moving industry, so it’s also important to ensure your supply chain can be easily iterated on to incorporate evolving legislation and market demand.

Data Powers BNPL

Regardless of trend, customer type, or region, your BNPL solution is powered by data. Diverse data sources pulled at the right time in the right order is the calling card of an optimized data supply chain. And an optimized data supply chain feeds your decisioning engine the information necessary to give you a smarter decision every time.

Building a data supply chain on your own, however, can be a huge undertaking and an even bigger headache. Instead, consider choosing a data partner that can build it for you, while connecting you to the integrations you need to grow your BNPL business.

Ideal features include:

- One data contract that gives you access to multiple data sources

- A single API to replace numerous integrations

- A wide variety of data types and sources, including alternative data

- Expert data source curation customized to your needs

- Simplified, no-code data supply chains that non-technical users can control

- Global data access

- Integrates into your decisioning technology to ensure seamless and smarter decisions

Do you want your data on-demand? Meet Provenir Data.

LATEST BLOGS

The Summer Skyline (UK)